Source: https://studentaid.gov/manage-loans/forgiveness-cancellation/public-service/questions

The Department of Education has updated their PSLF FAQ section, but it since it requires expanding the answers, we thought it’d be helpful to have the fully expanded version available for text searches.

Qualifying Employer – Q&As

What counts as a government employer for the PSLF Program?

Any U.S.-based government organization at any level (federal, state, local, or tribal) is considered a government employer for the PSLF Program. This includes employers such as the U.S. military, public elementary and secondary schools, public colleges and universities, public child and family service agencies, and special governmental districts (including entities such as public transportation, water, bridge district, or housing authorities).

A government contractor isn’t considered a government employer.

However, if you work as a contracted employee for a qualifying employer in a position or provide services which, under applicable state law, cannot be filled or provided by a direct employee of the qualifying employer you may be eligible for PSLF.

You can visit the PSLF Employer Search to verify your employer’s eligibility for the PSLF Program.

Note: Service as an elected member of the U.S. Congress is not qualifying employment for PSLF.

Which not-for-profit organizations qualify as eligible employers for the PSLF Program?

Eligible not-for-profit organizations include

- an organization that is tax-exempt under section 501(c)(3) of the Internal Revenue Code, and

- an organization that is not tax-exempt under section 501(c)(3) of the Internal Revenue Code, but that provides a qualifying service.

However, if the organization is a labor union or a partisan political organization, it isn’t an eligible PSLF employer.

Eligible not-for-profit organizations include most private elementary and secondary schools, private colleges and universities, and thousands of other organizations. Your employer can tell you if it is a not-for-profit organization and what its tax status is.

You can also visit the PSLF Employer Search, to verify your employer’s eligibility for the PSLF Program.

A not-for-profit organization that is not exempt under section 501(c)(3) of the Internal Revenue Code must provide a qualifying public services.

- Emergency management

- Military service

- Public safety

- Law enforcement

- Public interest law services

- Early childhood education

- Public service for individuals with disabilities and the elderly

- Public health

- Public education

- Public library services

- School library or other school-based services

What determines whether I am considered to be a direct employee of a qualifying employer?

Generally, the Internal Revenue Service (IRS) Form W-2 (Wage and Tax Statement) that you receive at the end of each tax year, identifies the employer you are a direct employee of. The Federal Employer Identification Number (FEIN or EIN) that is included in box b of the W-2 is what you will use to see if your employer is a qualifying employer in the PSLF Employer Search. Note: a 1099 is not the same as a W-2 and would indicate that you are receiving “non-employee compensation” which is generally an employee status that is not eligible for PSLF.

However, some employers will contract with a third-party organization called a Professional Employer Organization (PEO) to perform specific payroll and benefit functions as your co-employer. If your employer uses a PEO, it is the PEO’s EIN that will appear on your W-2 but, for PSLF purposes, you are considered a direct employee of your non-PEO co-employer so you will need to use the EIN of your non-PEO employer to search our database and have the non-PEO employer certify your employment.

On the other hand, if the employer that provides you with a W-2 is not a PEO, but rather a contracted organization, you would be a direct employee of that employer and it would be the EIN on your W-2 you would use in the PSLF Employer Search, even if you are performing your job for a different organization. See following Q&A on an exception relating to contract employment.

I’m employed full-time by a company that is doing work for a qualifying PSLF employer under a contract. However, the company that I work for is not a qualifying PSLF employer. Does this employment qualify for PSLF?

Generally, no. You must be a direct employee of a qualifying employer for your employment to qualify. This means that employees of contracted organizations, that are not themselves a qualifying employer, won’t qualify for PSLF including government contractors and for-profit organizations.

However, an exception exists if you work in a state that has laws that prevent an otherwise qualifying employer from hiring employees directly to fill positions or provide services. This is most common in states that have laws preventing health care facilities from hiring employees directly, so they contract with physicians’ groups to provide services. If this is the case, the contracted employee should report the EIN of the qualifying employer on their PSLF form (not their direct employer whose EIN appears on their W-2 or 1099) and have an authorized official of the qualifying employer certify their employment as an employee filling a position or providing a service that cannot be filled or performed by a direct employee due to state law.

A “contracted employee” can include an individual practicing as a sole proprietorship or as a partner, owner, or employee of a partnership, group, or professional corporation. The contracted organization may be a for-profit entity and employees may receive an IRS W-2, a 1099, and other tax forms from the contracted organization, depending on how it is organized.

The qualifying employer can sign the certification if either of the following is true:

- The borrower is or was employed under a contract or by a contracted organization in a position that, under applicable state law, cannot be filled by a direct employee of the organization, or

- The borrower is or was providing services that, under applicable state law, cannot be provided by a direct employee of the organization.

I’ve heard that my employment now qualifies because I work under a contract or for an organization contracted with a qualifying employer because my state does not allow them by law to directly hire employees performing the services I do, does my employment before this change count also?

Yes. If you submit a PSLF form certified by a qualifying employer now that your employment qualifies, it will be reviewed under the new rules regardless of the dates that are being certified on the form. This means that past employment certified by an authorized official of a qualifying employer today will count toward your PSLF eligibility.

Remember: in this situation you would use the EIN of the qualifying employer (not the EIN that appears on your W-2 or 1099) and have an authorizing official from the qualifying employer certify your employment under this condition.

What types of public service jobs will qualify me for loan forgiveness under the PSLF Program?

The specific job that you perform doesn’t matter, as long as you’re employed by a qualifying employer. For example, if you’re a full-time employee of a public school system, your employment would meet the requirements for PSLF, regardless of your position (teacher, administrator, support staff, etc.).

Note that this also means that if your employer is not a qualifying employer (i.e., a for-profit organization) your employment would not meet the requirements for PSLF, regardless of what public services your employer might provide.

I am a teacher who does not teach over the summer break. If I make payments during the summer, do those payments count toward PSLF?

Payments you make during the summer will count if you have a contract for an employment period of at least eight months and you work an average of 30 hours per week during that period, and if your employer still considers you to be employed full-time during the summer break. Of course, the payments must otherwise meet all PSLF requirements. In this circumstance, you should include the dates of the summer break when reporting your dates of employment on the Public Service Loan Forgiveness (PSLF) & Temporary Expanded PSLF (TEPSLF) Certification & Application (PSLF form), even though you aren’t actually teaching during that period. You may use the PSLF Help Tool to assist you with completing the PSLF form to certify employment.

I am an adjunct professor that is paid based on contact hours how do I convert those hours to determine if I work full-time for PSLF?

If you are a non-tenure or adjunct faculty member at an institution of higher education and are paid solely for the credit hours you teach, you meet the definition of full-time if you are employed the equivalent of 30 hours per week as determined by multiplying each credit or contact hour taught per week by at least 3.35.

What is full-time employment for PSLF?

For PSLF purposes, you are considered a full-time employee if you work an average of 30 hours or more per week during the period being certified on your PSLF form regardless of whether your employer considers you full-time for other purposes.

When determining your average number of hours per week, vacation or leave time provided by your employer are counted as hours worked. This includes leave taken for a qualifying condition under the Family and Medical Leave Act of 1993.

I previously submitted a PSLF form and my employer reported I was part-time but the new rules would allow my employment to be considered full-time for PSLF, can I correct this?

Yes. PSLF forms are reviewed under the rules in effect at the time the form is reviewed regardless of the employment dates on the form. This means that if your employment was previously certified as part-time because you did not meet your employer’s definition of full-time but worked 30 or more hours during your employment, you can submit a new PSLF form for the same period of time and the new definition of full-time would be used to determine your payment counts.

I’m working for more than one employer during the same period of time, but I’m not employed by either on a full-time basis. Will my combined employment be considered full-time for PSLF?

Yes, as long as the combined number of hours you work for each employer equals at least 30 hours per week. Each employer must be a qualifying employer for the employment to be included in determining whether you are employed on a full-time basis. For example, if you worked for one qualifying employer for 10 hours per week and you concurrently worked for a second qualifying employer for 20 hours per week, this would meet the 30 hours per week requirement.

I know that employment with a public school qualifies for PSLF. What about employment with a private school?

Most private elementary and secondary schools, and private colleges and universities, are not-for-profit organizations. If a private school has this status, it would qualify as a qualifying employer. However, a private school, college, or university that operates for profit is not a qualifying employer.

Can I receive PSLF if I have more than one employer over the course of 10 years?

Yes, and the employment does not even need to be consecutive. However, you must submit a PSLF form showing that you were employed full-time by a qualifying employer at the time you made each of the required 120 payments. You may use the PSLF Help Tool to assist you with completing a PSLF form.

I work for a religious organization, am I eligible for PSLF?

Yes. Religious organizations are recognized by the IRS as 501(c)(3) organizations and are therefore eligible for PSLF. However, these employers do not always register their tax-exempt status with the IRS so they may not appear in our employer database when you first search for your employer using the Employer Identification Number (EIN) that appears on your W-2. To ensure your employer is added to our employer database correctly, we ask that you upload your W-2 when you manually create a case for employer eligibility review. However, if your employer provides you with an IRS form 1099 (instead of a W-2), you are considered a ‘contract employee’ and would not be eligible for PSLF. Your employer should include all hours for which you are compensated, regardless of which activities you are performing, to determine if you are employed full-time or part-time when certifying your employment.

If I’m employed by a 501(c)(3) organization, but I work outside the United States, would the employment qualify under the PSLF Program?

Yes. Full-time employees of 501(c)(3) organizations may perform their work anywhere.

I’m a full-time employee of a foreign not-for-profit organization that is not a 501(c)(3) organization, but it provides a qualifying public service. Will my employment with this not-for-profit organization qualify for PSLF?

It depends on whether the organization operates in the United States.

If the organization operates in the U.S., your employment would qualify for PSLF purposes. If the organization does not operate in the U.S., your employment does not qualify.

Does employment by a foreign government or international, intergovernmental organization (such as the United Nations, Organization for Economic Cooperation and Development, Organization of American States, North Atlantic Treaty Organization) qualify for PSLF?

No. Only U.S. federal, state, local, and tribal government organizations, agencies, or entities are qualifying employers for purposes of PSLF. However, if you work for a U.S. delegation to an international, intergovernmental organization, such as the U.S. mission to the United Nations, your employment qualifies because your employer is the U.S. government.

I’m employed full-time by a qualifying employer in one of the islands that have a legal relationship with the U.S. Will that employment qualify for PSLF purposes?

Yes. American Samoa, the Commonwealth of Puerto Rico, Guam, the Virgin Islands, the Commonwealth of the Northern Mariana Islands, the Republic of the Marshall Islands, the Federated States of Micronesia, and the Republic of Palau are considered part of the U.S. for PSLF. Some employers on these islands use Employer Identification Numbers (EINs) that may not be recognized by our PSLF Employer Search. If you search for your employer using the EIN on your W-2 and receive a message that the EIN is invalid, you can submit a manual PSLF form with your W-2 and your form will be reviewed.

Does full-time volunteer service for a qualifying employer count toward PSLF?

No. Unless you are an AmeriCorps or Peace Corps volunteer, you must be a full-time employee who is hired and paid by a qualifying employer.

I am serving a fellowship with a qualifying employer. Does this qualify for PSLF?

It depends on the terms of your fellowship. It would qualify only if you are considered an employee who is hired and paid and issued a W-2 by the qualifying employer where you are serving the fellowship.

I’m the only official who can certify my employment. Can I certify my own qualifying employment?

Yes, you may certify your own employment if you are the only employee of the organization who can do so. However, we will request additional documentation concerning your employment, such as earnings statements, IRS W-2 forms, your application for tax-exempt status, or any other documentation required to be filed with the IRS on a periodic basis regarding the activities of the organization.

What if I make my last qualifying payment while working for a qualifying employer, but then leave that job to work for a for-profit organization before applying for the PSLF benefit. Am I still eligible for PSLF?

No. To be eligible for forgiveness after making 120 qualifying payments, you must be employed full-time by a qualifying employer at the time you make each qualifying payment and at the time you apply for loan forgiveness. Therefore, if you leave your job at a qualifying employer after meeting the PSLF eligibility requirements but before you apply for loan forgiveness, you will not be eligible for forgiveness since you must be working for a qualifying employer at the time you apply for forgiveness. However, you could regain eligibility if you later find full-time employment at another qualifying employer and then apply for loan forgiveness.

I genuinely work for a qualifying organization, but another organization generates my IRS Form W-2 under a contract with the qualifying organization. Does my employment qualify for PSLF?

Yes. If the organization that issues your W-2 is doing so only under an agreement to provide payroll or other administrative services for the qualifying organization, and the qualifying organization considers you to be an employee of that organization, then your employment qualifies for PSLF.

When certifying your employment, you should provide information about the qualifying organization you work for, not the organization that issues your W-2. An official of the qualifying organization should certify your employment.

If asked to submit documentation of your employment, such as a W-2, the qualifying organization and the other organization should write a joint letter explaining the employment arrangement between the qualifying organization and the other organization, and confirm in the letter that you are considered to be an employee of the qualifying organization.

I am an employee of an organization that is wholly owned by a not-for-profit organization. The organization I work for is not a not-for-profit organization, itself, but the not-for-profit organization that owns it treats my organization as a “disregarded entity” under Internal Revenue Service rules. Is my organization considered to be a not-for-profit organization for the purposes of PSLF?

Yes. If you are an employee of an organization that is a disregarded entity of a not-for-profit organization under Internal Revenue Service rules, then, for the purposes of PSLF, your organization is a not-for-profit organization regardless of how it is organized under state law (for example, as a Limited Liability Company).

If your employer is a disregarded entity of a 501(c)(3) organization, then it will automatically qualify. However, if your organization is a disregarded entity of another type of federally tax-exempt organization, such as a 501(c)(4) organization or a 501(c)(6) organization, then your organization must also provide a qualifying service to be considered a qualifying employer.

Eligible Loans

I made qualifying PSLF payments on my Direct Loans and then consolidated those loans. Do the payments I made before consolidation still count toward PSLF?

If you consolidate your loans, the qualifying payments made on the Direct Loans (other loan types will not be considered) included in your consolidation loan will be credited to your consolidation loan using a weighted average of those payments. Borrowers are strongly encouraged to certify all their qualifying employment applicable to the loans before they are consolidated to ensure that weighted average is correctly applied.

As part of the payment count adjustment, ED will allow qualifying payments from all loans included in a Direct Consolidation Loan, including FFEL Program and Perkins loans, to contribute toward the qualifying payment count on the Direct Consolidation Loan. The payment count adjustment will not use a weighted average. See the payment count adjustment for additional details.

Are private education loans eligible for PSLF?

No. Private education loans aren’t eligible for PSLF and can’t be consolidated into a Direct Consolidation Loan.

Are Direct Loans that are in default eligible for PSLF?

No. Defaulted Direct Loans are not eligible for PSLF and payments made while the loan was in default cannot count toward the 120 required payments. However, a defaulted loan may become eligible for PSLF if you resolve the default. Learn how to get your loan out of default.

Can my and my spouse’s Joint Consolidation Loan from the Federal Family Education Loan (FFEL) Program be consolidated into a Direct Consolidation Loan so that one or both of us can qualify for PSLF?

Due to recent changes to the law, borrowers will soon be able to separate joint consolidation loans. We’re working on implementing these changes and will provide updates on our Joint Consolidation Loan Separation News and Updates page.

I have a Joint Direct Consolidation Loan that I obtained with my spouse. Can we receive PSLF?

Yes, but your and your spouse’s employment history will be reviewed individually, and any forgiveness granted would be for the portion of the remaining loan balance attributable to the original loans of the spouse who has met the 120 qualifying months of qualifying employment requirement. If you both reach this requirement at the same time, the entire remaining balance would be forgiven. However, if one spouse reaches 120 qualifying payments first, only that spouse’s portion of the loan would be forgiven, and the remaining balance would continue to be the responsibility of both spouses. When, or if, the second spouse reaches 120 qualifying payments, the remaining balance would be forgiven.

While not necessary to qualify for PSLF, Joint Direct Consolidation loan borrowers will also be able to separate their loans based on the recent change to the law. We’re working on implementing these changes and will provide updates on our Joint Consolidation Loan Separation News and Updates page.

For example, if you were employed full-time by a qualifying employer when each of the required 120 payments was made, but your spouse never worked for a qualifying employer or worked for a qualifying employer only when some of the payments were made, the amount forgiven after the 120th qualifying payment would be the remaining balance of the loan attributable to the loans you originally received that were paid off by the joint consolidation loan. Both you and your spouse would remain responsible for repaying the remaining balance of the loan that is attributable to the loans your spouse originally received.

You can’t receive forgiveness of a joint Direct Consolidation Loan by combining payments made while only you met the employment requirement with payments made while only your spouse met the employment requirement.

For example, if only you were working for a qualifying employer when 80 payments were made and only your spouse was working for a qualifying employer when 40 payments were made, the payments cannot be combined to count as 120 qualifying payments that would make the loan eligible for PSLF.

Are Direct PLUS Loans eligible for PSLF?

Yes. Direct PLUS Loans are made to graduate or professional students and to parents of dependent undergraduate students. Like other Direct Loans, Direct PLUS Loans are eligible for PSLF. However, there are additional factors to consider if you are a parent who has taken out a PLUS loan.

First, your PSLF eligibility is based on your qualifying employment, not on the employment of the dependent student on whose behalf you borrowed.

Second, PLUS loans made to parents may not be repaid under any of the income-driven repayment plans, the repayment plans that are best for borrowers seeking PSLF. However, if you consolidate a PLUS loan that you took out on behalf of your child, you may then repay the new Direct Consolidation Loan under an income-driven repayment plan called the Income-Contingent Repayment Plan. You can’t repay under the Revised Pay As You Earn, Pay As You Earn, or Income-Based Repayment plans.

Note: PLUS loans made to graduate and professional students (as well as Direct Consolidation Loans that repaid PLUS loans made to graduate and professional students) may be repaid under any of the income-driven repayment plans.

Qualifying Payments – Q&As

Do I need to make consecutive payments to qualify for PSLF?

No. The 120 payments do not have to be consecutive payments. For example, if you have a period of employment with a non-qualifying employer, you won’t lose credit for prior qualifying payments you made. However, a payment can be counted only if you are employed full-time by a qualifying employer at the time you make the payment.

If I pay more than my scheduled monthly student loan payment amount, can I get PSLF sooner than 10 years?

No. You must make payments to cover 120 separate monthly obligations. Paying extra won’t make you eligible to receive PSLF sooner.

You may prepay, or make lump-sum payments, which first apply to any months during which you missed a payment and then would apply to future months up to your next income-driven payment (IDR) plan certification date or 12 months.

For example, if you recertified your IDR and your monthly payment was $100, but you paid $1200 for the first month’s payment, that payment would count as 12 separate monthly payments for that year. You would not need to make another payment until the next 12-month cycle when you have to re-certify your income for IDR. These payments would count as qualifying payments toward PSLF forgiveness once you certified your employment with a qualifying employer for the same 12-month period (which you can’t do in advance).

If I return to school and qualify for an in-school deferment on my Direct Loans that are in repayment, can I decline the deferment and make qualifying PSLF payments while I’m in school?

Yes. You can decline an in-school deferment on your loans that are in repayment status and make qualifying payments on those loans while you are in school. In this case, you must contact your servicer and request that the in-school deferment be removed. Remember, in order for your payments to qualify for PSLF, you must be employed full-time by a qualifying employer while you attend school.

Note: If you receive new Direct Subsidized Loans or Direct Unsubsidized Loans when you return to school, you won’t be able to make qualifying PSLF payments on those loans while you are in school. Any new Direct Subsidized Loans or Direct Unsubsidized Loans you receive won’t enter repayment until the end of the six-month grace period after you leave school. Although you could voluntarily make payments on your new Direct Subsidized Loans and Direct Unsubsidized Loans while you are in school or during your grace period, those payments wouldn’t count toward PSLF.

Can I waive the six-month grace period on my Direct Subsidized Loans and Direct Unsubsidized Loans and begin making qualifying PSLF payments early?

No. The law that governs the Direct Loan Program does not allow borrowers to waive the grace period on Direct Subsidized Loans and Direct Unsubsidized Loans. You cannot begin making qualifying PSLF payments until after your loans have entered repayment at the end of the grace period. Any payments you make on a loan during the grace period will not count toward PSLF. However, if you want to immediately begin making qualifying payments on your federal student loans as soon as you leave school, you may consolidate your loans into a Direct Consolidation Loan during your grace period and enter repayment right away.

I’m thinking of serving as a Peace Corps or AmeriCorps volunteer and plan to request a deferment or forbearance on my Direct Loans. If I’m not making payments during my service period, can I receive credit toward PSLF?

AmeriCorps or Peace Corps volunteers should specifically request an Economic Hardship Deferment as time spent in an Economic Hardship deferment during your volunteer service will count as payments toward PSLF.

You may also use the transition payment you receive after completing your Peace Corps service—or the Segal Education Award you may receive after AmeriCorps service—to make a lump-sum payment on your Direct Loans and receive credit for a certain number of payments for PSLF into the future (up to your next income-driven payment (IDR) plan certification date or 12 months). This number is determined by dividing the amount of your lump-sum payment by your scheduled full monthly payment amount, for a credit of no more than 12 qualifying monthly payments.

However, instead of taking an Economic Hardship Deferment, you could choose to make qualifying PSLF payments under an income-driven repayment (IDR) plan during your service period. For some borrowers performing volunteer service, the required monthly payment amount under an IDR plan may be as low as $0.

I’m receiving student loan repayment benefits through one of the U.S. Department of Defense’s Student Loan Repayment programs. Do those payments count toward PSLF?

If your military service qualifies for a military-related deferment or forbearance, we suggest that you take advantage of that deferment or forbearance as that time will count as payments toward PSLF.

For each lump-sum payment made by the U.S. Department of Defense (DOD) toward your Direct Loans as part of one of the student loan repayment programs it administers, you will receive credit for up to 12 future qualifying payments for PSLF if you also have qualifying employment during those future months.

First, the lump-sum payment is applied to any months that you missed a payment and then to future months. The number of payments for which you receive future credit is determined by dividing the amount of the lump-sum payment by your scheduled full monthly payment amount. This benefit is available only for lump-sum payments made on or after July 1, 2016.

If my scheduled monthly payment under an income-driven repayment plan is $0, does each month during which my payment is $0 count toward the required 120 separate, monthly payments?

Yes. Any month when your scheduled payment under an income-driven repayment plan is $0 will count toward PSLF if you also are employed full-time by a qualifying employer during that month.

If I make partial payments more frequently than monthly (for example, twice each month, when I get paid), will my payments count toward PSLF?

If you make multiple partial payments that total at least your monthly payment amount, the series of partial payments will satisfy the monthly requirement and count as a one qualifying payment for PSLF.

For example, if your required monthly payment is $200 and you make two $100 payments you would receive credit for one qualifying payment.

I was in a deferment or forbearance in the past that does not count for PSLF, and I worked for a qualifying employer at the same time. Is there anything I can do to get PSLF credit for that time?

The payment count adjustment may credit you with certain periods of deferment or forbearance without you taking any action. We encourage you to wait until after the payment count adjustment is completed in 2024 as many periods of deferment and forbearance will be automatically credited to you without requiring you to pay money for that time.

If a period of deferment or forbearance is not covered by the payment count adjustment, then you may want to consider a buyback. If you have a single month (or multiple months) in your payment history that do not count as a qualifying payment because you were in a deferment or forbearance status other than those that are considered an eligible payment equivalent, you can buyback that month to make it a qualifying payment. To do so you must make an extra payment of at least as much as what you would have made under an income-driven repayment (IDR) plan that you were eligible for each month that you were in a deferment or forbearance and also had qualifying employment. If you have consolidated your loans, you can only buyback time on the consolidation loan and not from the loans included in the consolidation loan or for any period prior to the consolidation loan. If your loan is paid-in-full, forgiven, or discharged, you can’t buyback on that loan.

Buyback will be available for periods of forbearance or deferment on loans with a positive outstanding balance as long as the period of deferment or forbearance overlaps with qualified employment. You can confirm that the loan was in a forbearance loan status or deferment loan status by logging in to your StudentAid.gov account and reviewing your loan in My Aid. Borrowers cannot buyback periods during which their loan was in an in-school or in-grace loan status through StudentAid.gov.

Federal Family Education Loan (FFEL) Program loans, Perkins Loans, other non-Direct Loans or any loan included in a Direct Consolidation Loan will not be eligible for buyback. Only periods of deferment or forbearance on Direct Loans with a positive balance where the deferment or forbearance also overlaps with qualified employment will be eligible. You can check that your loan has a positive balance by reviewing both the outstanding principal balance and outstanding interest balance for your loan on StudentAid.gov. Any Direct Loan where either the outstanding principal balance or the outstanding interest balance is greater than zero will be eligible.

ED will be posting more information on StudentAid.gov describing the specific circumstances for which a borrower can request a buyback and how to submit a request in the summer 2023. Borrowers will be required to confirm that their complete qualifying employment history is certified in addition to providing copies of their tax returns for any calendar year during which they plan to request a buyback. We encourage borrowers that are considering requesting a buyback to check their employment history and to begin gathering their tax return information now. Borrowers should not contact the PSLF servicer requesting a buyback or hold harmless request until we have posted additional details on StudentAid.gov.

Qualifying Repayment Plans – Q&As

I’m repaying my Direct Consolidation Loan under the Standard Repayment Plan. Does that plan qualify for PSLF?

Generally, no. The Standard Repayment Plan for Direct Consolidation Loans is not the same repayment plan as the 10-year Standard Repayment Plan, and payments made under the Standard Repayment Plan for Direct Consolidation Loans do not usually qualify for PSLF purposes.

Under the Standard Repayment Plan for Direct Consolidation Loans, the maximum repayment period varies from 10 years to 30 years, depending on the amount of the consolidation loan and the amount of your other education loan debt. This longer repayment period generally results in a lower monthly payment than the monthly payment amount required under the 10-year Standard Repayment Plan. Payments made under the Standard Repayment Plan for Direct Consolidation Loans would qualify for PSLF purposes only if the maximum repayment period was set at 10 years, and that would be the case only if the total amount of the consolidation loan and your other education loan debt was less than $7,500.

If you are seeking PSLF, the best option would be to repay your Direct Consolidation Loan under an income-driven repayment plan.

What other Direct Loan repayment plans would give me a monthly payment that is at least equal to the payment that would be required under a 10-year Standard Repayment Plan?

Under the Graduated Repayment Plan, payments start out lower and then gradually increase, generally every two years. Therefore, payments made during the later portion of the repayment period under the Graduated Repayment Plan may in some cases equal or exceed the payment amount that would be required under a 10-year Standard Repayment Plan, and these payments would count for PSLF.

If I’m repaying my Direct Loans under the PAYE or IBR Plan and my monthly payments are no longer based on my income, will my payments continue to count for PSLF?

Yes. Although you’ll always initially have a payment based on your income in the Pay As You Earn (PAYE) and Income-Based Repayment (IBR) plans, under certain circumstances your monthly payment under those plans may no longer be based on income. However, your monthly payments will continue to qualify for PSLF if you remain on the PAYE or IBR plan.

I’m in the process of rehabilitating a defaulted Direct Loan. Will my rehabilitation payments count toward PSLF?

No. Payments made while in default or to rehabilitate a defaulted Direct Loan do not qualify for PSLF.

PSLF Process – Q&As

After I submitted the PSLF form, I was notified that I now have a new servicer for my federal student loans. Why did my servicer change?

The PSLF servicer administers PSLF for all Direct Loan borrowers. As a result, if you submit a PSLF form and the PSLF servicer determines that your employment qualifies, all of your Direct Loans as well as any of your FFEL Program loans that are held by the U.S. Department of Education will be transferred to the PSLF servicer.

What kind of documentation do I need to keep to show that I worked for a qualifying PSLF employer while making the required 120 payments on my Direct Loan(s)?

The PSLF servicer will confirm that your employer is a qualifying employer based on the information provided on the PSLF form that you submit. In some cases, the PSLF servicer may require additional documentation about your qualifying employment. Therefore, you should keep records that identify your employer, show your dates of employment with that employer, confirm that you were a full-time employee, and demonstrate that your employer meets the definition of a qualifying employer. For example, documents that would support your employment are IRS W-2 forms and pay stubs. You should retain as many documents supporting your qualifying employment as possible.

You should submit the PSLF form (and additional documentation, as required) on a regular basis, and keep copies for your records.

How do I submit a PSLF form?

You may use the PSLF Help Tool to

- complete your PSLF form,

- send your form to your employers for their digital signature (and certifying your employment), and

- electronically submit your form to the PSLF servicer for processing.

While using the help tool, you will need to provide the correct email address for an authorizing official to receive an email from us requesting they certify your employment and digitally sign the form. Tell your employer to expect an email sent from DocuSign (dse_NA4@docusign.net) on behalf of the Department of Education’s office of Federal Student Aid. Once digitally signed, your form will be electronically submitted to the PSLF servicer for processing.

You may also submit a PSLF form by downloading the PDF after going through the PSLF Help Tool. While in tool, choose manual signature and on the next page select the View in My Activity button. From the My Activity page, download your form, print it, sign it, and have your employer(s) sign your form.

If you prefer not to use the PSLF Help Tool, you can download and print a blank PDF of the form, complete all sections, sign it, and have your employer(s) sign it. See submission instructions for manually completed PDFs below.

What method of signing is acceptable for manual PSLF form submission?

Digital signatures from you or your employer must be hand-drawn (from a signature pad, mouse, finger, or by taking a picture of a signature drawn on a piece of paper that you then scan and embed on the signature line of the PSLF form) to be accepted. Typed signatures, even if made to mimic a signature, or security certificate-based signatures are not accepted.

| Signature Examples | |

|---|---|

| Signature Type | Yes/No |

| Hand drawn from signature pad, mouse, or finger | ✔ |

| Typed using a cursive font or any other font | X |

| A scanned photo of a signature that was hand-drawn on paper | ✔ |

| Digital certificate-based signature | X |

| A wet signature that was drawn in ink and sent to us in its original format | ✔ |

I made some qualifying payments, but I no longer work for a qualifying employer and do not think I will work in qualifying employment again. Can I receive partial forgiveness based on the number of qualifying payments that I made?

No. There is no partial loan forgiveness. To receive PSLF, you must make all 120 qualifying payments while working for a qualifying employer. Since these payments do not need to be consecutive, the qualifying payments you have already earned will not disappear in case you do become employed by an eligible employer in the future.

When I submit my form for loan forgiveness after making the required 120 qualifying payments, how long will it take to process my form and forgive my remaining loan balance?

Processing times will vary depending on factors such as whether you previously submitted documentation of employment for review or submitted documentation only at the time you applied for loan forgiveness, the number of your employers, any gaps in your employment or payment history, and any required follow-up.

If you periodically submitted the PSLF form so that your eligibility could be tracked while you were making the required 120 payments, your form for loan forgiveness will likely be processed more quickly.

Once the PSLF servicer has received all of the documentation needed to determine whether you qualify for loan forgiveness, you will be notified.

You should continue to make payments while your PSLF form is being processed, but you have the option to request a forbearance if you believe (or our system determines) you have already made 120 payments. If you requested a forbearance while your form is under review, those months would not count toward your 120 payments if it is determined you have not earned forgiveness. Any payments you make beyond the 120 that are required would be refunded to you if it is determined you qualify for forgiveness.

What will happen if my PSLF form is approved?

If your PSLF form is approved for forgiveness, you will be notified that the entire remaining balance of your eligible Direct Loans will be forgiven, including all outstanding interest and principal. If you made payments after your 120th qualifying payment, those payments will be treated as overpayments and refunded to you.

What will happen if my PSLF form is denied?

If we determine that you are not eligible for loan forgiveness, you will be notified of this determination and will be provided with the reason(s) you were determined to be ineligible. You will then be required to resume making payments on your loans according to the terms of your Master Promissory Note.

If you do not qualify for forgiveness, interest that accrued (accumulated) during the period when your form was being evaluated will be added to your outstanding balance but not be capitalized.

Note: Sometimes you may be able to submit documentation or make additional qualifying payments to resolve the circumstances of the denial for PSLF. Contact the PSLF servicer to discuss this option.

I received a letter from the PSLF servicer saying that my loans, employment, or some or all of my payments don’t qualify toward PSLF. What do I do if I think my loans, employment, or payments do qualify?

Carefully read the letter, including the description of the eligibility requirements, to understand why your loans, employment, or payments didn’t qualify for PSLF. Review the relevant sections of our PSLF page. If you still have questions, contact the PSLF servicer at 1-855-265-4038.

After you understand why the PSLF servicer believes that your loans, employment, or payments don’t qualify for PSLF, you can always submit additional information showing that your loans, employment, or payments do in fact qualify for PSLF. The PSLF servicer will reconsider its decision based on that additional information. You may also submit a request for reconsideration.

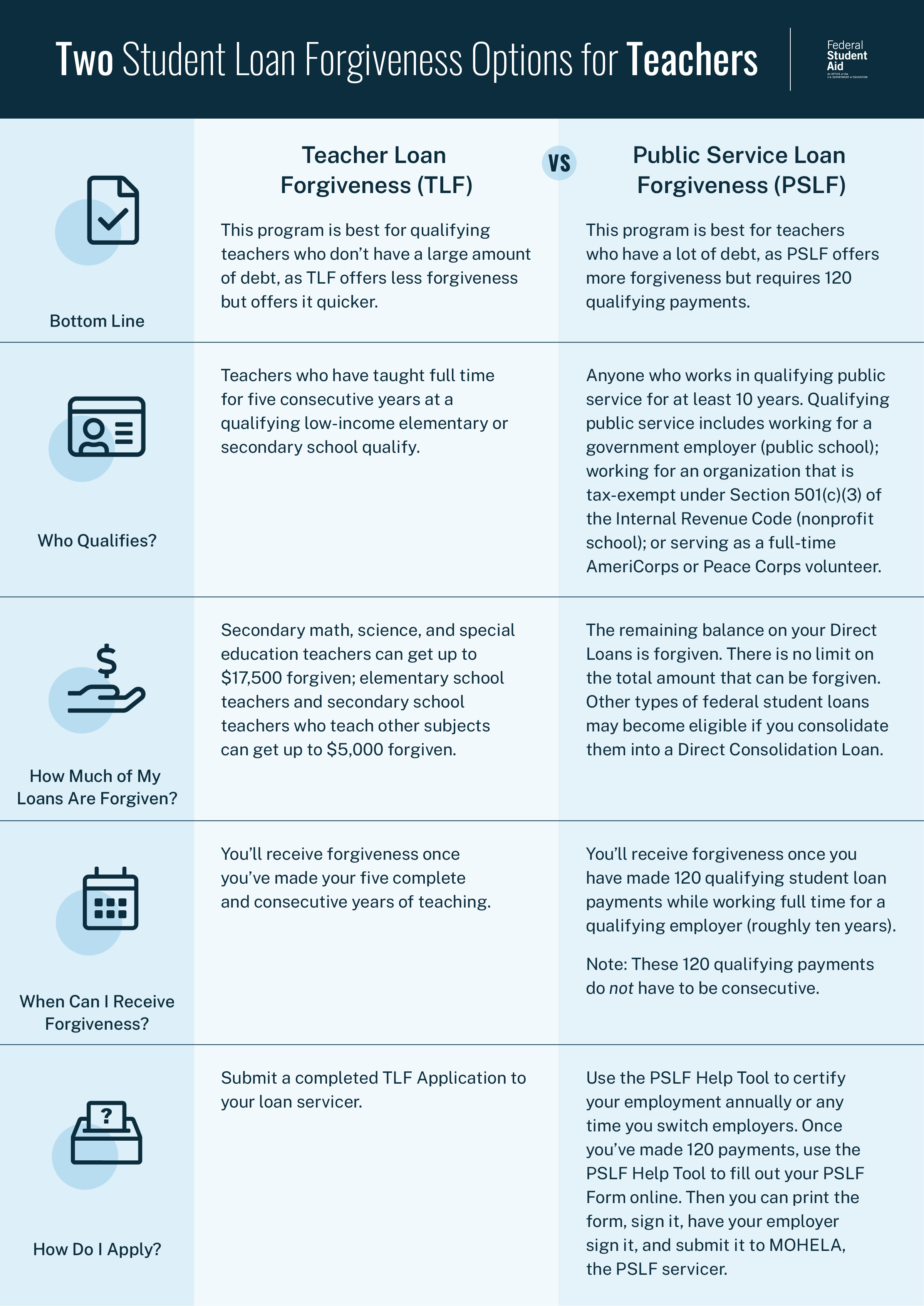

If I receive loan forgiveness under the federal Teacher Loan Forgiveness Program after completing five years of qualifying teaching service, will I also be able to qualify for PSLF?

Yes. However, you can’t receive a benefit under both the Teacher Loan Forgiveness Program and PSLF for the same period of teaching service. For example, if you make payments on your loans during your five years of qualifying employment for Teacher Loan Forgiveness and then receive loan forgiveness for that service, the payments you made during that five-year period will not count toward PSLF. This graphic (and text-only version) explains the two loan forgiveness options for teachers.

{kind=link}

If I’m employed by a qualifying employer and receive a student loan repayment benefit from my employer under the Federal Student Loan Repayment Program or under another employer-based student loan repayment program, can I also receive PSLF based on the same employment?

Yes. You may receive benefits under both an employer loan repayment plan, including the Federal Student Loan Repayment Program and the PSLF Program for the same period of qualifying public service.

If your employer makes a single lump-sum payment that covers multiple months of your student loan payments, the lump-sum payment will only count up to 12 months of repayment or your next recertification date whichever is sooner.

Learn more about the Federal Student Loan Repayment Program.

If I receive PSLF forgiveness and then return to school after a couple years, would I qualify for forgiveness on the new loans because I already earned forgiveness through ten years of public service or would I need to complete another ten years of service to be eligible for forgiveness?

Once a borrower has successfully applied for PSLF and received forgiveness on current, eligible loans, a borrower cannot borrow new loans in the future and apply previously qualified employment history to forgive the newly borrowed loans. A loan taken out in the future would require an additional 120 months of qualifying payments to be forgiven.

Forgiveness through the PSLF program is applied at the loan level. Each loan a borrower is repaying must have 120 qualifying payments before being eligible for forgiveness. This may result in a borrower having multiple loans entering repayment at different times having different forgiveness dates depending on when each loan entered repayment. Moreover, qualifying employment must be matched to eligible payments while the loan is in repayment for that payment to be a qualifying payment, therefore previous employment cannot be applied to future repayment periods.